Pay by Bank: Recurring payments beyond traditional Direct Debit

Insurance

Utilities

Financial Services

Telcos

.png)

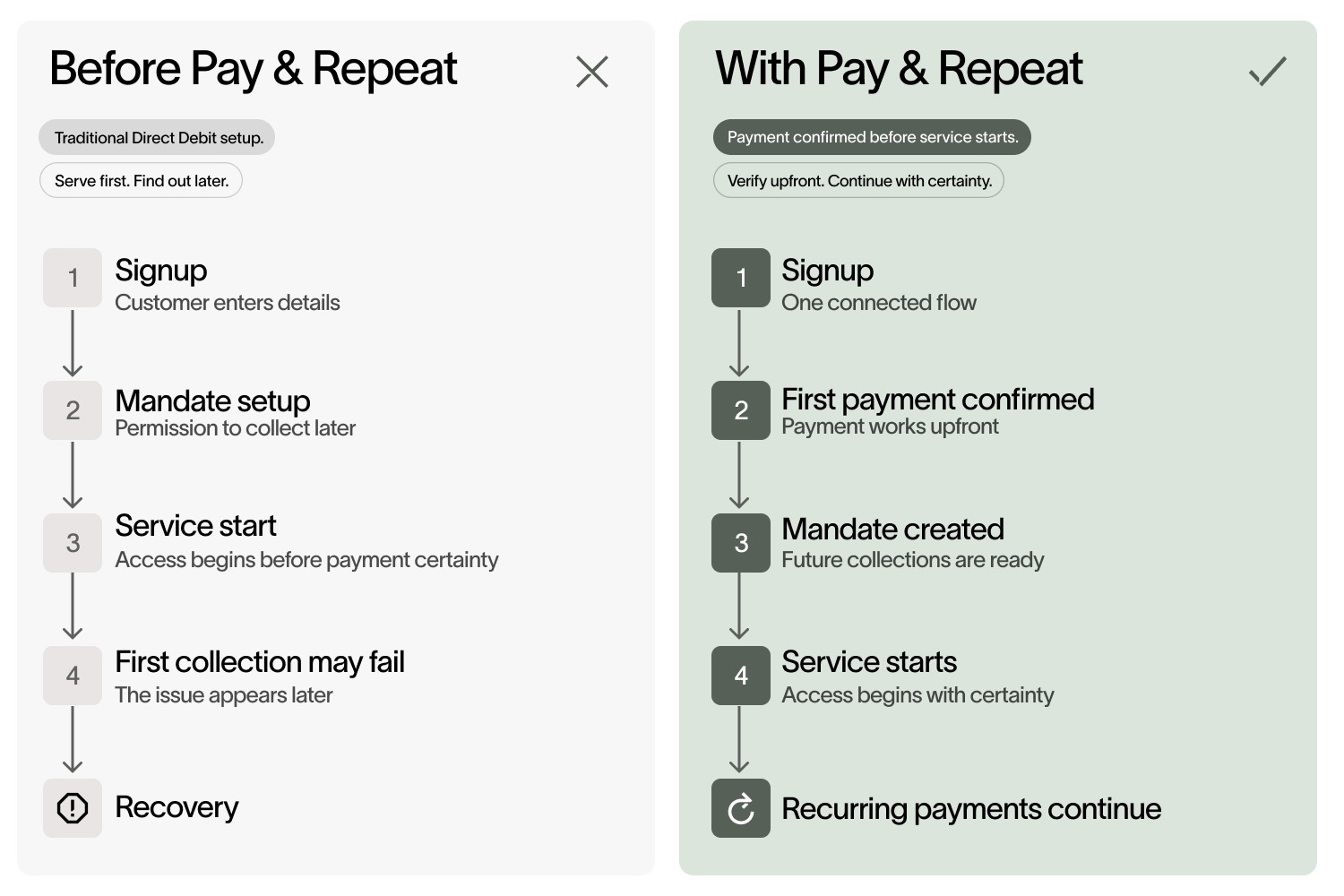

Traditional Direct Debit flows were never built for instant digital onboarding. While a mandate confirms permission to collect future payments, it cannot confirm that the first payment will actually succeed at the moment a customer signs up.

That creates the problem of blind mandate acceptance: merchants can have a valid mandate but still lack certainty that the first payment will succeed.

That is where Pay & Repeat changes the game. By combining an upfront Pay by Bank payment with instant Direct Debit mandate creation, merchants can secure the first payment while simultaneously locking in the long-term recurring relationship.

Key takeaways:

- Merchants using tranditonal Direct Debit-only flows at signup have a valid mandate but no certainty the first payment will succeed.

- Pay & Repeat locks the first payment and recurring mandate in a single flow, removing the risk of a mandate existing without a confirmed first payment.

- Connecting first payment and mandate setup in one journey reduces incomplete onboarding and orphaned mandates.

- Open Banking enables the first payment to happen directly from the customer’s bank account, without card details or a separate deposit.

Traditional Direct Debit: Reliable but lagging at signup

In a traditional Direct Debit-only flow, a customer submits their details, a mandate is processed, and the merchant gains permission to pull future payments.

For established customers, this works perfectly. But at signup, it leaves an expensive gap of uncertainty.

A Direct Debit mandate gives the merchant permission to collect later once the submitted details have been validated, and the mandate has been created. But it does not confirm that the first collection will succeed, or that funds will be available when the collection is attempted.

That delay is not new. It has been part of how SEPA Direct Debit works from the start. Because Direct Debit is a “pull” payment, the collection is processed after the mandate is created, with lead time built into the flow. The result is a window of uncertainty between signup and first payment confirmation.

For recurring merchants, that window matters.

The customer may expect immediate access. The merchant may want to start the service quickly. But the first payment outcome is still unknown.

That creates a familiar trade-off: start the relationship and accept payment risk, or wait for confirmation and add friction to the onboarding journey.

- For utilities it can lead to failed first payments becoming arrears from day one.

- For insurers it can mean payment failure at policy signup where the first premium creates uncertainty around policy activation.

Pay & Repeat bridges that gap by confirming the first payment upfront while creating the Direct Debit mandate for future collections – all in the same flow.

How Pay & Repeat changes the flow

Pay & Repeat combines two actions in one customer journey: an upfront Pay by Bank payment and Direct Debit mandate creation.

- The customer makes the first payment through Pay by Bank, powered by Open Banking, or through a relevant local payment method such as iDEAL or Wero, depending on the market. At the same time, the mandate for future recurring payments is created. Core capabilities include instant confirmation, market-specific local payment methods such as:

- Swish

- iDEAL

- Bancontact

- Wero

A single modular API, and a locked relationship between the first payment and the mandate.

That last point matters. In a disconnected setup, a customer might complete one step but not the other. Pay & Repeat is designed to keep the first payment and recurring mandate connected in one flow, reducing the risk of incomplete onboarding or abandoned mandates.

For the merchant, the result is a stronger starting point. The first payment is confirmed upfront, and the future recurring relationship is set up at the same time.

For the customer, the experience is simple: sign up, pay, and continue.

Direct Debit vs Pay & Repeat

This is not about saying Direct Debit is outdated. It is about using Pay by Bank to improve the moment where traditonal Direct Debit-only flows can leave merchants exposed.

Why Open Banking and local payment methods matter here

Open Banking makes this combined approach possible by allowing the upfront payment to happen directly from the customer’s bank account. But the principle is broader than one payment method. In some markets, Pay & Repeat can also support local payment methods such as iDEAL and Wero, helping merchants meet customers through familiar bank-based payment experiences.

That creates a faster, more connected setup journey without relying on card details or a separate deposit flow. The customer can confirm the first payment upfront, while the mandate for future Direct Debit collections is created in the same onboarding journey.

Bank-based payment experiences are also becoming more familiar. In the UK, the Financial Conduct Authority reported in 2025 that Open Banking payments had grown 53% year on year, with variable recurring payments accounting for 16% of all Open Banking transactions.

For recurring payment merchants, the point is not that every market will move in the same way or use the same payment method. The point is that account-to-account based payment experiences are becoming more normal, and that opens the door to better onboarding flows.

Pay & Repeat evolves to address the practical recurring payments challenge: how to confirm the first payment without losing the benefits of Direct Debit for future collections.

What happens in the customer journey

In a traditonal Direct Debit-only journey, the customer usually submits the information needed to create a mandate, then waits. The merchant may activate the service immediately, but the payment outcome is still unknown. If the first collection fails, the business has to recover the payment after the customer relationship has already started.

In a Pay & Repeat journey, the first payment and mandate setup happen together. The customer chooses a Pay by Bank or local payment method, confirms the first payment, and sets up future recurring payments in the same flow.

For payments teams, that means fewer disconnected steps to monitor. For finance teams, it means the first cash event is clearer. For customers, it removes the awkward gap between signing up and knowing whether the service is actually ready to start.

How it works across different industries

- Utilities:

Pay & Repeat can help reduce the risk of starting a customer relationship with arrears. The first payment is confirmed before the business relies on future collections. This matters because utilities are focused on reducing payment failures, improving reconciliation and lowering operational cost across high-volume billing journeys. - Insurers:

It can support a cleaner start to the policy relationship. When the first premium is confirmed upfront, there is less uncertainty around early payment failure and policy continuity. - Telcos and broadband:

The value is especially clear in complex onboarding journeys. Broadband, mobile and handset contracts often require identity checks, address verification, payment setup, Direct Debit mandate creation and, in some cases, upfront charges. When those steps are disconnected, customers drop off and operations teams inherit the rework.

Virgin Media O2’s Open Banking onboarding flow shows what changes when these steps are brought together: broadband and mobile sign-ups were reduced to a single digital flow, nearly 60% of users chose automated Direct Debit via Open Banking, and the business saw fewer failed payment setups and less back-office rework. - Lenders and BNPL providers:

Pay & Repeat can strengthen the first repayment moment. Before credit is drawn or exposure increases, the business has a clearer signal that the customer can complete the first payment.

A better model for recurring payment onboarding

The future of recurring payments solutions is a hybrid approach – a combination of Direct Debit and Open Banking.

Direct Debit remains valuable for ongoing collections. Pay by Bank adds upfront confirmation where the risk is highest. Pay & Repeat brings those two strengths together in one flow: first payment confirmed, mandate created, and the recurring relationship ready to continue.

For payments leaders, that means fewer failed-first-payment surprises. For finance leaders, it means stronger cash flow visibility and less recovery work. For customers, it means a simpler start.

Recurring payment onboarding should not begin with guesswork. It should begin with confirmation.

Frequently asked questions

What is the difference between Direct Debit and Pay by Bank?

Direct Debit is designed for recurring collections. The customer submits the information needed to create a mandate. Once that mandate is created, the merchant has permission to collect future payments from the customer’s bank account, usually on a scheduled basis.

Pay by Bank is designed for direct, real-time bank payments. The customer confirms a payment through their bank, giving the merchant faster payment confirmation.

For recurring payments, the two can work together. Pay by Bank can confirm the first payment upfront, while Direct Debit sets up future repeat collections.

Which industries benefit most from combining Pay by Bank with Direct Debit?

The strongest fit is for businesses that need both immediate payment certainty and ongoing recurring collections.

That includes utilities, insurers, telcos, lenders, and subscription businesses. Utilities can reduce the risk of new customers starting in arrears. Insurers can confirm the first premium before the policy relationship moves forward. Telcos can simplify onboarding and reduce failed payment setups. Lenders can reduce uncertainty before the first repayment. Subscription businesses can give customers fast access while setting up future payments.

How does Open Banking support recurring payment onboarding?

Open Banking supports recurring payment onboarding by connecting customers directly to their bank during signup.

That can reduce manual entry, help verify account details, and enable an upfront Pay by Bank payment before future Direct Debit collections begin. Instead of separating first payment and mandate setup into different steps, Open Banking can bring them into one connected journey.

For merchants, that means more certainty at signup. For customers, it means a smoother start.

Related Articles

Raise conversion today with fast, frictionless payments.

Get in touch with our sales team to explore how we can help you meet goals and transform your payment experience.